Is Taking a Loan Good or Bad? Here is the Honest Truth

A few months ago, a close friend of mine called me in a panic. He wanted to buy a new car—something sleek to look good on his weekend trips. His salary was decent, but he didn’t have the cash upfront, so he was about to sign the papers for a massive 7-year car loan. He asked me, “Bhai, loan lena sahi hai ya galat?” (Is taking a loan right or wrong?)

I told him exactly what I tell everyone: A loan is like a sharp kitchen knife. If a professional chef uses it, they create a masterpiece. If a careless person handles it, they cut their own hand.

In India, we have been raised with the mindset that debt is a sin. Our parents always told us, “Jitni chadar ho, utne hi pair pasaro” (Stretch your legs only as far as your bedsheet extends). But in today’s financial world, completely avoiding loans isn’t always smart, and blindly taking them is dangerous.

Let’s skip the confusing banking jargon and break down how loans actually work in real life, so you can decide what’s best for you.

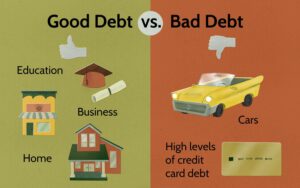

Good Debt vs. Bad Debt: Yes, There is a Difference!

The biggest mistake people make is grouping all loans into one category. To understand debt, you need to understand whether it is putting money into your pocket in the long run, or just draining your bank account.

1. What is Good Debt?

Good debt is an investment that grows in value or helps you generate more income over time.

- Home Loans: Real estate usually appreciates. Instead of paying lifetime rent, you are building an asset that becomes entirely yours.

- Education Loans: Borrowing money to upgrade your skills or get a degree increases your future earning potential. It’s an investment in yourself.

- Business Loans: Taking money to expand your shop, buy inventory, or scale operations to generate more profit is a calculated, smart move.

2. What is Bad Debt?

Bad debt is money borrowed to buy things that lose value the moment you buy them, or things you don’t actually need.

- Personal Loans for Vacations: Borrowing money to fund an exotic beach holiday might give you great Instagram photos, but the memories won’t pay off the high-interest EMIs next month.

- Credit Card Roll-overs: Buying expensive clothes or gadgets on EMIs and only paying the “minimum due” is a financial trap. Credit card interest rates can go up to 40% annually!

Answering Burning Questions from Reddit

When you scroll through online forums like Reddit, you see thousands of real people asking the same anxious questions about loans. Let’s answer a few of them plainly:

“Should I take a loan to invest in the stock market or mutual funds?”

Absolutely not. This is the fastest way to go broke. The stock market is unpredictable. If the market crashes, your investment drops, but your bank doesn’t care—they will still demand their EMI on time. Never borrow money to gamble or speculate.

“Is a car loan good or bad?”

A car is a depreciating asset. The moment you drive it out of the showroom, its value drops by 10-20%. If you need a car for daily commuting or family utility, a small, manageable car loan is fine. But if you are taking a massive loan just to show off a luxury brand to your neighbors, it’s a terrible financial move.

My Personal Golden Rules Before You Sign the Loan Papers

Over years of tracking financial charts and talking to people drowning in debt, I’ve realized that people don’t get ruined by the loan itself—they get ruined because they didn’t do the math beforehand.

Before you take any loan, follow these three simple rules:

- The 40% Limit: Your total monthly EMIs (home loan, car loan, personal loan combined) should never cross 40% of your take-home salary. If you earn ₹50,000 a month, your total EMIs must stay below ₹20,000. If it crosses that, you are living on the edge.

- Check the Hidden Costs: Banks love to hide processing fees, documentation charges, and foreclosure penalties in the fine print. Always ask for the “Effective Interest Rate” or the total amount you will end up paying back.

- Always Calculate the “Total Interest” Trait: A bank might tell you, “Sir, your EMI is just ₹5,000 a month.” It sounds cheap, right? But if you pay that for 20 years, you might end up paying double the actual loan amount in just interest!

Don’t Rely on Guesswork: Calculate It Instantly

Whenever people plan to take a loan, they usually rely on the math provided by the bank agent. Never do that. The agent is trying to sell you a product; they want you to borrow more. You need an independent, unbiased calculation.

To avoid getting tricked, I highly recommend using the free loan calculator tool at toolist.xyz.

I recommend this specific tool because it doesn’t ask for your personal information, email, or phone number (so no annoying spam calls from agents the next day!). It is clean, incredibly simple, and shows you exactly what your monthly EMI will be, along with the total interest you will pay over the years.

Before you step into a bank, open toolist.xyz, adjust the slider with your loan amount, interest rate, and tenure, and look at the real numbers. It takes 10 seconds but can save you lakhs of rupees.

The Verdict

So, is taking a loan right or wrong?

It is completely right if it helps you build a secure future, buy a permanent roof for your family, or grow a business—provided you have a solid plan to repay it. It is completely wrong if it’s used to fund a lifestyle you cannot afford.

Be honest with yourself, look at your actual income, crunch the numbers safely on toolist.xyz, and only borrow what you can repay without losing your peace of mind!

You can use our online tools .

Thank you 😊